As geopolitical tensions are rising globally, financial planners recommend their clients to build a Core and Satellite portfolio using mutual fund schemes to optimise their long-term returns and meet their financial goals.

Let us understand Core and Satellite Portfolio in the accumulation stage

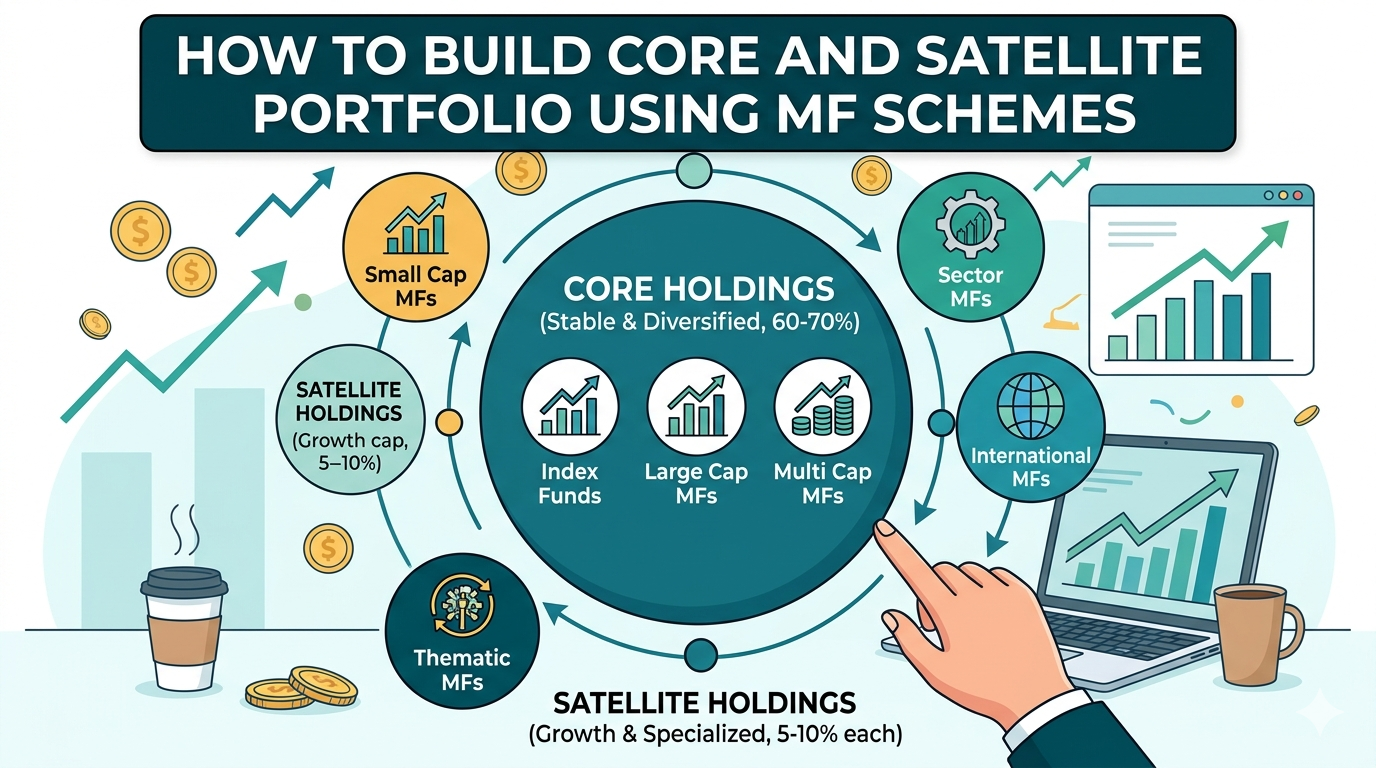

Core Portfolio using MF schemes:

The core portfolio is built based on the investor’s objectives—age, risk-taking capacity, and the time available (Time Horizon of investments) to reach their financial goals. It is called long term asset mix as well as strategic asset allocation

Investors can have a mix of low cost index funds and diversified large-cap-oriented equity funds that aim to provide stability and help achieve long-term goals. Large-cap stocks have proven track records and strong management teams with the ability to manage difficult domestic or global situations. To build the core equity portfolio, investors can use a mix of large cap schemes/Funds and Index funds. They can also invest in Flexi cap and Multi cap funds with proven track record and consistent returns as desired by investors.

Satellite Portfolio using MF schemes:

The satellite portfolio also called Tactical Asset allocation can be made based on relatively aggressive schemes /funds such as small-cap funds, momentum funds, value funds, or narrow Sectoral funds like defence, infrastructure, banking, IT, and pharma. These carry a higher risk but have the potential to generate higher alpha.

Core vs Satellite- How much to be in each strategy?

Based on an investor’s risk profile and timeframe for goals, financial planners believe investors can allocate a large amount 70–75% to their core portfolio, and the balance 25–30% to the satellite portion. While the core portfolio can remain stable and would not require high churning or frequent changes, the satellite portion may require investors to time the market to enter and exit at right time to generate maximum returns. Such schemes could carry higher risk and volatility

Now, it’s well known that equity has the best return potential, and if you are in the accumulation phase, it has a crucial role in your portfolio.

This does not mean that debt funds or hybrid funds can’t be core funds. A debt fund can be a core fund in a retiree’s portfolio. And if someone is looking for automatic asset allocation, even a hybrid fund can be a core fund.

The core funds take care of the returns and the stability, and the satellite funds help boost the overall returns or help diversify better

Dean Madhu Shina